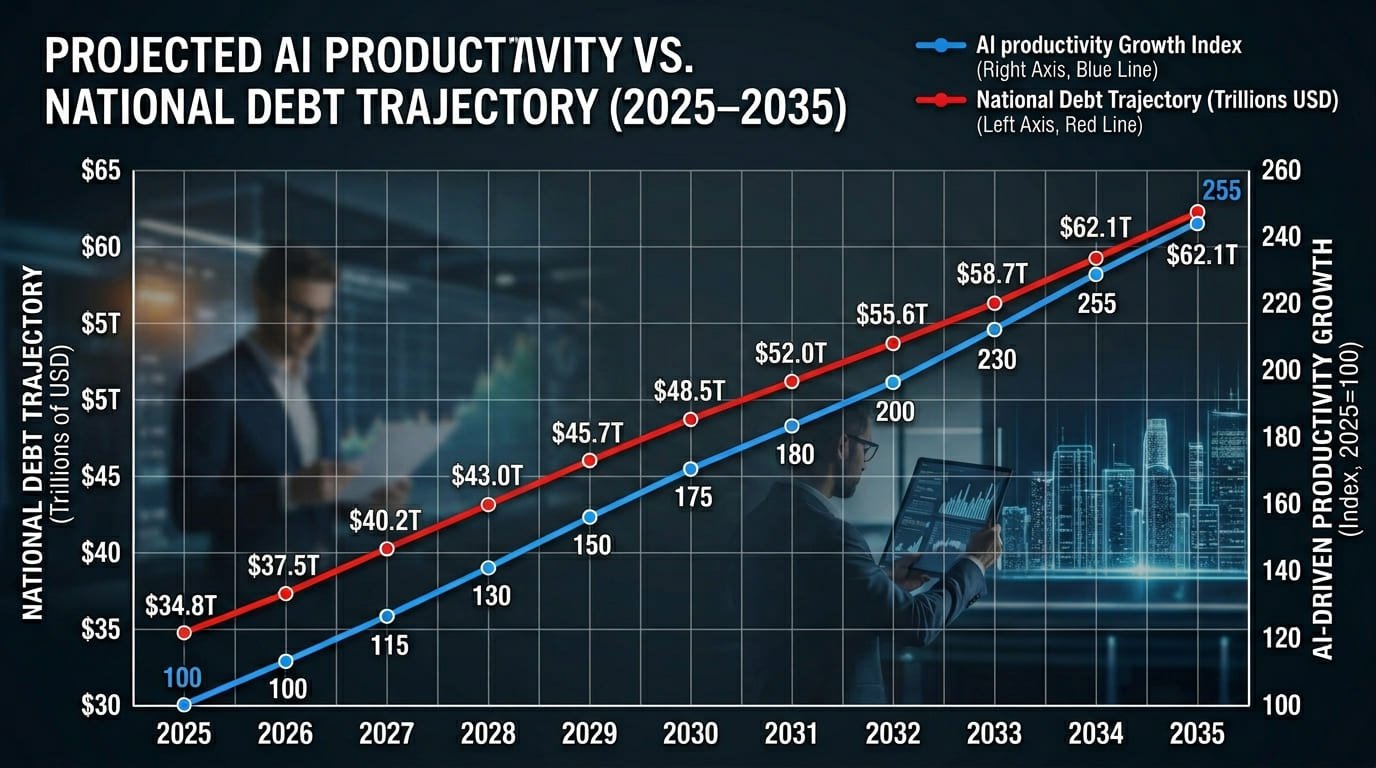

The AI productivity national debt impact is no longer a theoretical debate confined to economics journals. It is the defining fiscal policy question of 2026. With US national debt surpassing $39 trillion — exceeding 100% of GDP for the first time since World War II — and technology giants committing nearly $1 trillion in AI infrastructure investment, the question before policymakers, CFOs, and enterprise leaders is direct: can AI-driven productivity growth materially reduce America’s debt burden, or will the transition costs of automation deepen the fiscal crisis it is meant to solve?

A landmark May 2026 study by the Yale Budget Lab provides the most rigorous modeling yet of this question. The findings are simultaneously encouraging and cautionary. Under moderate AI adoption — defined as 2.5% annual labor productivity growth between 2025 and 2030, which aligns with the median forecast of surveyed economists — AI could stabilize the debt-to-GDP ratio, leaving it at approximately 100.3% in 2035, essentially unchanged from today. This is a materially better outcome than the baseline trajectory in which debt continues climbing toward 120% of GDP.

But the Yale Budget Lab’s executive director, Martha Gimbel, is direct about the limits of this optimism: AI is unlikely to be “some kind of free, infinite money tree.” The fiscal benefits of AI productivity are contingent on assumptions about labor markets, tax structures, interest rates, and the political choices governments make about supporting workers displaced by automation.

This analysis examines the full evidence base — drawing on Yale Budget Lab, Moody’s Analytics, the Federal Reserve Bank of San Francisco, the National Bureau of Economic Research, and Acemoglu’s foundational productivity research — to give executives and policymakers a rigorous, balanced, and actionable picture of the AI productivity national debt impact in 2026 and beyond.

[See our AI Economic Policy and Enterprise Strategy Framework]

| $39T US National Debt — May 2026 | 100.2% Debt-to-GDP Ratio Q1 2026 | 2.5% Yale Moderate AI Productivity Growth |

The Fiscal Baseline: Why AI Productivity National Debt Impact Matters Now

The United States national debt reached $39 trillion by May 2026, surpassing 100.2% of GDP — a threshold last crossed during World War II mobilization spending. Without structural intervention, Moody’s Analytics projects the federal debt-to-GDP ratio reaching 122.5% by 2036 under baseline conditions, with debt service costs consuming an increasing share of federal revenues.

This trajectory is not merely an accounting problem. It constrains fiscal policy flexibility, increases vulnerability to interest rate shocks, and creates compounding pressure on social program funding, defense investment, and infrastructure spending. The Congressional Budget Office’s long-run projections, updated through early 2026, show no stabilization pathway under current policy without either significant revenue increases, spending cuts, or an exogenous productivity shock of historic magnitude.

AI is that potential shock — but whether it materializes at sufficient scale and speed to alter the debt trajectory depends on factors that are neither automatic nor politically simple.

AI Productivity National Debt Impact: What the Research Actually Shows

The research landscape on AI productivity impact is rich, heterogeneous, and — critically — less uniformly optimistic than technology sector narratives suggest. A careful reading of the evidence reveals a wide range of credible estimates and meaningful uncertainty about the timeline and distribution of productivity gains.

Yale Budget Lab — May 2026

The most current and directly relevant modeling comes from the Yale Budget Lab’s May 2026 study. Working from a survey of economists, technologists, and policy analysts about AI’s expected impact on GDP, labor force participation, and productivity, the team modeled three scenarios:

| Scenario | Productivity Growth | Debt-to-GDP by 2035 | Job Displacement Assumed |

| Optimistic | 2.5% annual (2025–2030) | ~100.3% — Stabilized | Minimal displacement, full employment |

| Moderate +Support | 2.5% annual | Reduced vs baseline but rising | Significant displacement, generous support ($42,400/worker) |

| Moderate +Basic | 2.5% annual | Reduced vs baseline but rising | Significant displacement, basic support ($5,500/worker) |

| No AI Gains | Baseline only | 120%+ trajectory continues | No displacement assumed |

The critical finding: in every scenario where AI productivity gains materialize, the fiscal outcome is better than in a world without AI gains. But only the most optimistic scenario — high productivity with minimal displacement — is sufficient to stabilize debt as a share of GDP.

Moody’s Analytics — February 2026

Moody’s Analytics published a comprehensive macroeconomic consequences study in February 2026 that modeled AI’s impact across multiple productivity scenarios. Their base case projects the federal debt-to-GDP ratio at 100.6% in 2026, rising to 122.5% by the mid-2030s without structural change. Their modeling of AI productivity scenarios shows meaningful improvement in fiscal trajectories with sustained adoption, but confirms that AI alone is unlikely to reverse debt accumulation without complementary fiscal policy adjustments.

The Moody’s analysis also identifies an important transmission mechanism often overlooked in optimistic AI fiscal narratives: faster AI-driven economic growth could push interest rates higher, increasing government debt-servicing costs and potentially offsetting a portion of the productivity-driven fiscal benefit.

Acemoglu (2024) and the Skeptical Case

MIT economist Daron Acemoglu’s influential 2024 research provides the most prominent skeptical counterpoint. His modeling estimates AI’s boost to total factor productivity at an upper bound of 0.66 to 0.71% cumulatively over ten years — a modest figure that would produce minimal impact on the debt trajectory. Acemoglu’s concern centers on the concentration of AI productivity gains in narrow task categories and the substantial time required for economy-wide diffusion.

This skeptical position receives some empirical support from a February 2026 NBER study of nearly 6,000 CEOs and CFOs across the US, UK, Germany, and Australia, which found that the vast majority of executives report little observable AI impact on their operations. Among those using AI, usage averaged only 1.5 hours per week — suggesting that enterprise AI adoption remains far below the threshold required to generate macroeconomically significant productivity gains.

[Moody’s Analytics AI Macroeconomic Consequences Report — economy.com]

Three Structural Factors That Could Offset AI Productivity Fiscal Benefits

Factor 1 — The Displaced Worker Cost

The single most significant variable in every AI fiscal model is the cost of supporting workers displaced by automation. The Yale Budget Lab modeled two worker support scenarios: a generous program equivalent to US retiree spending at $42,400 per worker annually, and a basic program matching current unemployment spending at $5,500 per worker. In both cases, worker support costs materially reduce — but do not eliminate — the fiscal benefit of AI productivity gains.

Prominent political figures including Senator Bernie Sanders and OpenAI CEO Sam Altman have both proposed substantial worker support programs as a social response to AI-driven displacement. The fiscal math is unambiguous: the more generous the support infrastructure, the smaller the net fiscal benefit of AI productivity, regardless of how large those productivity gains are.

Factor 2 — The Tax Structure Problem

AI-driven automation creates a structural tax revenue problem that fiscal models must account for. As AI replaces labor with capital — automating tasks previously performed by workers who paid income and payroll taxes — income shifts from workers to capital owners. Capital income in the United States is taxed at structurally lower rates than labor income. This means that even if AI-driven automation increases total economic output, the federal government may collect a smaller share of that larger output than it would have under a labor-intensive economy.

This tax structure dynamic is not a reason to oppose AI adoption. It is a reason to design tax policy in parallel with AI adoption strategy — ensuring that the fiscal dividend from AI productivity is captured through the tax code rather than flowing entirely to capital owners.

Factor 3 — The Productivity Paradox

The Federal Reserve Bank of San Francisco’s 2026 analysis flags what it terms the productivity paradox of AI adoption: despite 374 S&P 500 companies mentioning AI in earnings calls with largely positive characterizations, and despite significant AI capital investment, broader macroeconomic productivity statistics show limited impact. Workers’ regular AI use increased 13% in 2025 according to ManpowerGroup’s Global Talent Barometer — but confidence in the technology’s utility fell 18%, indicating persistent implementation challenges.

The San Francisco Fed’s framing is instructive: current AI adoption resembles replacing a steam motor with an electric one but leaving the factory floor unchanged — good progress, but not transformative. True productivity transformation requires redesigning workflows and processes around AI capabilities, not simply layering AI tools onto existing operations.

Implications for Enterprise Leaders, CFOs, and Policymakers

For Enterprise CFOs and Strategy Leaders

The AI productivity national debt impact research has direct implications for enterprise investment strategy. The productivity gains required to materially alter the fiscal trajectory are economy-wide phenomena — they require broad, deep AI adoption across sectors, not concentrated gains in a handful of technology-intensive industries. Enterprise leaders who adopt AI strategically, redesign workflows around AI capabilities, and achieve genuine productivity gains contribute to the macroeconomic conditions that make the optimistic fiscal scenarios possible.

Conversely, enterprises that adopt AI superficially — deploying tools without process redesign, measuring outputs in AI tool usage hours rather than productivity outcomes — contribute to the productivity paradox dynamic that the SF Fed research identifies. The difference between economy-wide AI productivity transformation and economy-wide AI productivity disappointment is determined by millions of enterprise adoption decisions.

For Policymakers and Fiscal Authorities

The Yale Budget Lab research implies a clear policy framework for maximizing AI’s fiscal contribution. Policymakers should prioritize AI adoption infrastructure — research funding, regulatory clarity, education and retraining programs — that accelerates broad-based AI adoption while managing the distributional consequences of automation. Tax policy design must account for the labor-to-capital income shift that AI drives, ensuring fiscal revenue captures a sufficient share of AI-driven productivity gains. Worker transition support, while fiscally costly, is both ethically necessary and economically rational — displaced workers who remain permanently outside the workforce represent both a welfare failure and a lost productivity contribution.

For Sovereign Debt and Investment Analysis

For analysts evaluating US sovereign debt dynamics, the AI productivity variable introduces genuine scenario dispersion. Under the Yale Budget Lab’s optimistic scenario, the debt trajectory stabilizes at approximately today’s ratio through 2035 — a materially better outcome than the baseline projection. Under more pessimistic productivity scenarios, the baseline debt accumulation continues and may be compounded by AI-related transition costs. Prudent sovereign analysis should model a range of AI adoption scenarios rather than assuming either the most optimistic or most pessimistic outcome.

Conclusion: AI’s Fiscal Promise Is Real — But Conditional

The AI productivity national debt impact is real, measurable, and potentially transformative — but it is not automatic, inevitable, or free. The most rigorous 2026 research establishes a clear conditional structure: if AI adoption is broad and deep, if labor markets adjust without catastrophic permanent displacement, if tax policy captures the productivity dividend, and if worker transition support is efficiently designed, AI can stabilize America’s debt trajectory and create the foundation for sustainable fiscal improvement.

None of those conditions are guaranteed. The productivity paradox evidence — in which widespread nominal AI adoption has not yet produced observable macroeconomic productivity gains — is a warning that adoption and transformation are not the same thing. The enterprise leaders, policymakers, and institutions that understand this distinction and act accordingly will determine whether the $1 trillion in AI infrastructure investment translates into the fiscal dividend the optimistic models project.

Key actions for executives, CFOs, and policymakers:

- Stress-test your enterprise AI investment thesis against the NBER finding that most executives report minimal AI operational impact — are your AI deployments generating measurable productivity gains or nominal adoption metrics?

- Integrate AI productivity assumptions into long-range financial planning with explicit scenario modeling — do not treat optimistic AI fiscal scenarios as a baseline without evidence that your organization is achieving the underlying productivity gains.

- For policymakers: design worker transition investment and tax structure reform in parallel with AI adoption strategy — the fiscal benefit of AI is substantially determined by how these adjacent policy choices are made.

- Monitor the Yale Budget Lab and Moody’s Analytics modeling updates as 2025–2030 productivity data accumulates — the scenario you are in will become empirically distinguishable from alternatives within the next two to three years.

- For sovereign debt analysts: build AI productivity scenario dispersion into US fiscal outlooks rather than assuming either the optimistic or pessimistic tail — the evidence supports a wide central range.

The $39 trillion question is not whether AI can help reduce America’s national debt. The evidence says it can. The question is whether the structural conditions for that help will be built — or whether the productivity paradox will persist long enough to make the optimistic scenarios irrelevant.

Frequently Asked Questions (FAQs)

Q1: What is the AI productivity national debt impact?

The AI productivity national debt impact refers to the effect that AI-driven increases in labor and total factor productivity could have on a government’s fiscal position — specifically its national debt as a share of GDP. When AI raises productivity, it increases economic output and government tax revenues without proportional increases in spending, which can slow or reverse debt accumulation. The 2026 Yale Budget Lab study found that moderate AI productivity growth of 2.5% annually could stabilize the US debt-to-GDP ratio at approximately 100.3% by 2035, compared to a baseline trajectory exceeding 120%.

Q2: Can AI realistically reduce the US national debt?

Research suggests AI can slow national debt growth and potentially stabilize the debt-to-GDP ratio, but is unlikely to reduce the absolute dollar amount of debt in the near term. The Yale Budget Lab’s most optimistic scenario — strong productivity growth with minimal worker displacement — produces debt stabilization by 2035, not reduction. In all scenarios with significant worker displacement and government support costs, the debt continues to rise but more slowly than in a world without AI productivity gains. The key finding is that AI’s fiscal contribution is positive across all modeled scenarios, but the magnitude varies enormously depending on adoption breadth, labor market outcomes, and policy choices.

Q3: What is the Yale Budget Lab’s AI fiscal study and what did it find?

The Yale Budget Lab published a study in May 2026 modeling the impact of AI-driven productivity growth on the US national debt trajectory. Working from a survey of economists and technologists about expected AI impacts on GDP and labor force participation, the study modeled scenarios ranging from optimistic — 2.5% annual labor productivity growth with full employment — to more realistic scenarios involving significant worker displacement and government support costs. The study found that AI productivity gains improve fiscal outcomes in every scenario compared to no AI adoption, but that only the most optimistic scenario produces actual debt stabilization. Even in optimistic scenarios, AI is not a free fiscal remedy.

Q4: Why might AI hurt the national debt rather than help it?

Several mechanisms could cause AI adoption to worsen rather than improve the national debt trajectory. First, supporting large numbers of displaced workers requires significant government spending that can exceed productivity-driven revenue gains. Second, AI-driven automation shifts income from labor to capital, and capital is taxed at lower rates than labor in the US, potentially reducing federal revenue as a share of GDP even as total output grows. Third, faster AI-driven growth could push interest rates higher, increasing debt service costs. Fourth, if AI adoption is superficial — nominal rather than deep — productivity gains may be insufficient to offset these negative fiscal dynamics.

Q5: What does the productivity paradox mean for AI’s fiscal impact?

The productivity paradox refers to the gap between widespread nominal AI adoption and limited measurable macroeconomic productivity improvement. A February 2026 NBER study of nearly 6,000 executives found most report minimal AI operational impact; AI usage averaged just 1.5 hours per week. The Federal Reserve Bank of San Francisco describes current AI deployment as analogous to replacing a steam motor with an electric one without redesigning the factory — incremental improvement rather than transformation. If the productivity paradox persists, the favorable fiscal scenarios from the Yale Budget Lab and other optimistic models will not materialize, and the debt trajectory will follow the unfavorable baseline.

Q6: How does AI adoption speed affect the national debt trajectory?

Speed of AI adoption is a critical variable in fiscal impact modeling. Productivity gains that arrive in the 2025 to 2030 window have a materially different compounding effect on the debt trajectory than gains that arrive in the 2030 to 2040 window — earlier productivity gains reduce debt accumulation during a period when interest rates and debt service costs are elevated. Moody’s Analytics and Penn Wharton Budget Model research both show that front-loaded productivity gains — concentrated in the early 2030s — have disproportionately positive fiscal effects compared to slow, gradual adoption curves.

Q7: What role does tax policy play in determining AI’s debt impact?

Tax policy is a first-order determinant of whether AI productivity gains translate into fiscal improvement. As AI automates tasks previously performed by labor, income shifts from workers — who pay income tax and payroll tax — to capital owners, who pay lower effective tax rates on investment income. Without tax policy adjustments, this structural shift means the government captures a shrinking fraction of a growing economy, potentially worsening the fiscal position even as AI raises total output. Policymakers who design tax reform in parallel with AI adoption strategy — ensuring that productivity dividends are captured through the revenue system — can significantly improve the probability of achieving the favorable fiscal scenarios.

Q8: How should enterprises think about AI investment given the national debt context?

The AI productivity national debt impact research has a direct strategic implication for enterprise leaders: genuine, measurable productivity improvement from AI — not nominal adoption — is what drives both enterprise value creation and the macroeconomic conditions that benefit everyone. CFOs and strategy leaders should design AI investment programs around productivity outcome metrics — time savings per process, error rate reduction, output per employee — rather than AI tool deployment counts. Enterprises that achieve real productivity gains contribute to the broad-based adoption conditions that the optimistic fiscal scenarios require. Those that adopt superficially contribute to the productivity paradox that makes those scenarios increasingly unlikely.

| Article by Waqas Raza | vitaloralife.com | Published for an international executive audience (US & Global) |